The Quiet Rise of “Usage-Based Insurance”: Why Your Behavior Now Shapes Your Premium

Insurance is no longer just about who you are—it’s increasingly about how you behave. A growing trend called usage-based insurance (UBI) is quietly reshaping how premiums are calculated, using real-time data to personalize pricing in ways that weren’t possible even a few years ago.

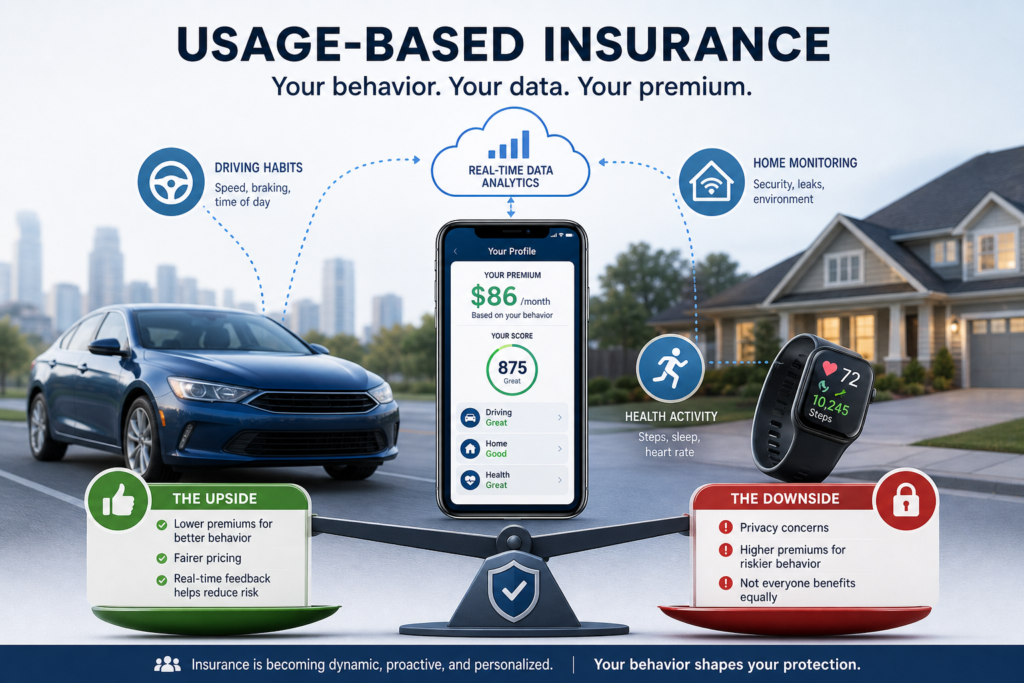

What Is Usage-Based Insurance?

Traditionally, insurers relied on broad categories—age, location, and history—to estimate risk. But today, advances in data collection and analytics allow insurers to go much deeper.

Usage-based insurance uses real-world behavioral data such as:

- Driving habits (speed, braking, time of day)

- Home monitoring (security systems, leak detectors)

- Health activity (wearables tracking steps, sleep, heart rate)

This shift reflects a broader industry move toward granular, data-driven underwriting, where risk is assessed continuously rather than statically.

Why Insurers Are Embracing It

Several recent trends are pushing insurers in this direction:

1. Rising Costs Demand Precision

Inflation has increased repair, medical, and replacement costs, forcing insurers to raise premiums overall.

More precise pricing helps insurers stay competitive while managing risk.

2. Climate and Catastrophe Risk

Global insured losses from natural disasters are now exceeding $100 billion annually, pressuring insurers to better understand individual risk exposure.

3. Consumer Price Sensitivity

As premiums rise—home insurance alone has increased significantly in recent years—customers are more willing to trade data for lower rates.

What This Means for Consumers

Usage-based insurance creates a new trade-off: personalization vs. privacy.

The upside:

- Safer drivers and healthier individuals can get lower premiums

- Policies feel more “fair” because they reflect actual behavior

- Real-time feedback can help reduce risk (e.g., safer driving habits)

The downside:

- Constant data tracking raises privacy concerns

- Riskier behavior may lead to higher premiums than before

- Not all consumers benefit equally (e.g., night-shift workers driving late)

The Bigger Picture: Insurance Is Becoming Dynamic

This trend signals a deeper transformation: insurance is shifting from a reactive product (pay after loss) to a proactive system (monitor and prevent risk in real time).

We’re moving toward a world where:

- Your car insurer “knows” how you drive

- Your home insurer monitors potential damage before it happens

- Your health insurer rewards preventative behavior

At the same time, studies show that while the market is becoming more competitive in some segments, insurers are applying increasingly granular risk segmentation—meaning no two customers are priced exactly the same anymore.

Final Thought

Usage-based insurance isn’t just a pricing tweak—it’s a fundamental shift in how risk is understood. The question going forward isn’t whether this model will grow (it will), but how consumers and regulators will balance fair pricing, transparency, and privacy in a data-driven insurance landscape.