The Hidden Shift in Personal Insurance: Why Your Premium Keeps Rising (and What It Means)

If your insurance bills feel higher than they used to, you’re not imagining it. Across the U.S., personal insurance—from auto to homeowners to health—is undergoing a quiet but significant transformation. Recent studies and industry observations point to a simple reality: insurance is becoming more expensive, more personalized, and more dependent on data than ever before.

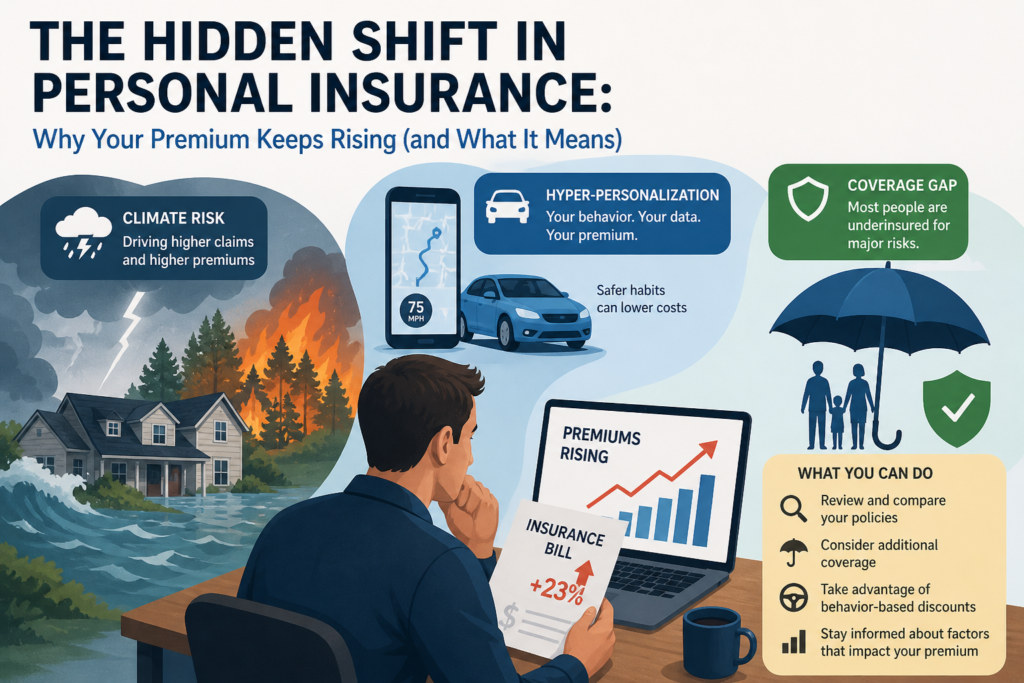

1. Rising Costs Are the New Normal

Over the past few years, insurance premiums have surged across nearly every category. Home insurance, for example, has increased dramatically—by as much as 57% between 2019 and 2024 in some analyses . Health insurance costs are also climbing, with family coverage reaching nearly $27,000 annually in 2025 .

What’s driving this? A combination of inflation, higher repair and medical costs, and an increase in claims—especially those tied to severe weather and accidents. Climate-related disasters alone have pushed insured losses into the tens of billions, forcing insurers to raise premiums to stay solvent .

2. Climate Risk Is Reshaping Coverage

One of the biggest emerging trends is the growing impact of climate risk on personal insurance. More frequent wildfires, storms, and floods are making certain regions more expensive—or even difficult—to insure.

In some high-risk areas, insurers are pulling back coverage entirely or tightening underwriting standards. This creates a ripple effect: fewer options for consumers and higher prices for those who remain insured. Even outside high-risk zones, premiums are rising as insurers spread the cost of these disasters across all policyholders.

3. Insurance Is Becoming Hyper-Personalized

At the same time, insurance is becoming more tailored to individual behavior. Technologies like telematics (used in auto insurance) track driving habits such as speed, braking, and mileage. Safer drivers can earn lower premiums, while riskier behavior leads to higher costs .

Artificial intelligence is also playing a growing role. Insurers now analyze large datasets—including claims history and behavioral patterns—to price policies more precisely. This means two people with similar demographics could pay very different rates based on their personal risk profile.

4. The Coverage Gap Problem

Despite rising risks, many people remain underinsured. Studies show that while a large majority of individuals worry about lawsuits or catastrophic losses, only a small percentage carry sufficient umbrella or excess liability coverage .

This gap is becoming more dangerous as legal settlements grow larger and unexpected risks—like cyber threats or liability claims—become more common. In today’s environment, basic policies may no longer provide enough protection.

5. What This Means for You

The takeaway is clear: personal insurance is no longer a passive purchase. It’s something that requires active management.

Consumers today should:

- Regularly review and compare policies (switching insurers is becoming more common)

- Consider additional coverage, especially umbrella policies

- Take advantage of behavior-based discounts (like safe driving programs)

- Understand how external factors—like climate and inflation—affect their premiums

Final Thought

Personal insurance is evolving from a standardized product into a dynamic, data-driven system. While this brings opportunities for savings and customization, it also places more responsibility on individuals to understand their coverage.

In a world where risks are increasing—and becoming less predictable—being informed about your insurance may be just as important as having it.